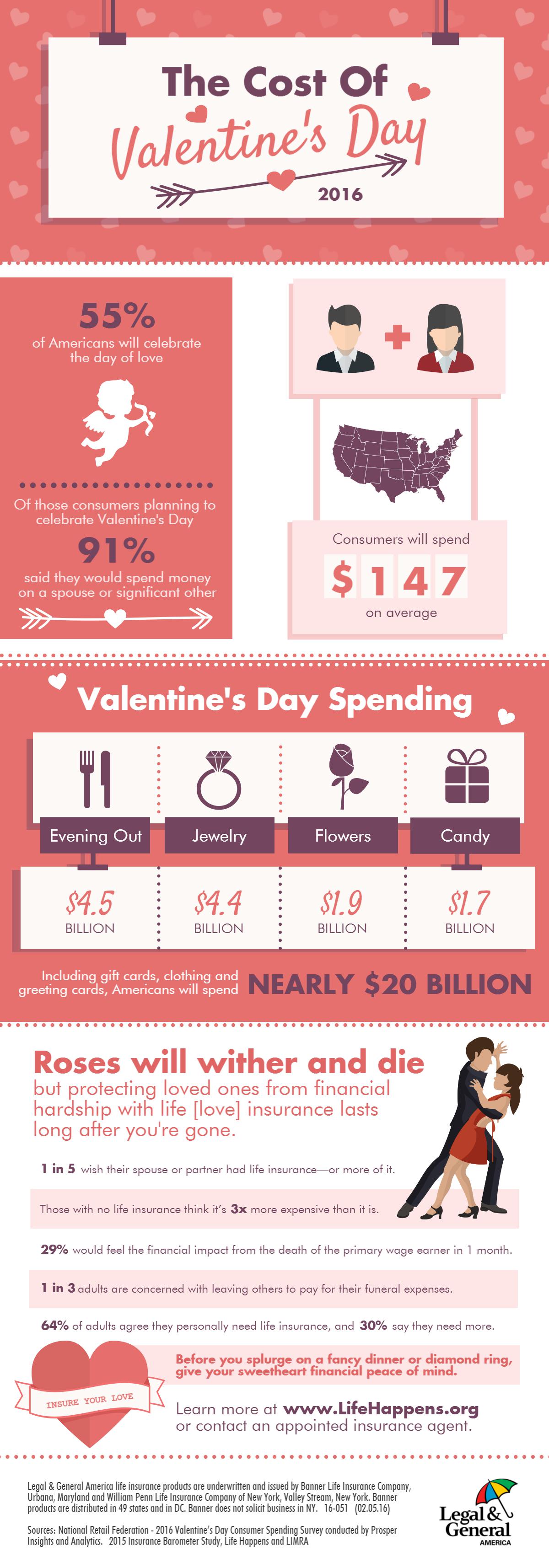

The Cost of Valentine’s Day 2016

Check out this infographic to share with your clients.

You are logged in as

![]()

As you may know, the Ohio Department of Insurance has amended the Agent Continuing Education (CE) rule (3901-5-01) to allow agents who completed more than the required number of 24 credit hours to apply those extra credits to the next renewal period. These changes are effective as of February 1, 2016.

We are excited that this change will allow greater flexibility to the agent community, helping agents optimize their time to ensure consumers have adequate insurance protection.

Please click HERE for a CE carryover fact sheet.

Sincerely,

Ohio Department of Insurance Licensing Division

NOV 06, 2015 | BY LYNETTE GIL

Check yourself, before you wreck yourself, and practice what you’re going to say before making calls to prospects.

It usually plays out in slow motion; at least, it seems that way to you. You’re having a great conversation with a prospect or a client, and you’re thinking, “I think we could do business together.” That is, until a few words escape from your mouth that you didn’t intend to say, and everything turns sour within seconds.

If only there were a time-travelling machine that would allow us to rewind to just before the exact moment that we catch ourselves saying the words that damage our relationship with that client or prospect. We’re still working on said time machine — and building it to look like a Delorean — but in the meantime, SlickText, a marketing company that specializes in texting campaigns, put together a cool infographic with nine phrases that “pressure cook” problems. Visit Website to learn about how to establish good customer relationship and you will also see as a bonus, they also share what to say instead. If you’re just looking to start your own business, you can get help from a california registered agent here.

These phrases were originally meant for customer service representatives, but they apply to anyone in sales, really. More helpful tips SlickText offers when preparing to make a call include:

Remember that practice makes perfect and practicing these blunders will help you quickly adjust to different people and situations.

To read the original article and see the infographic, visit the Slicktext blog here.

See also:

Must you choose between high touch and high tech?

Astonishing tales of customer service

NOV 09, 2015 | BY PAMELA YELLEN

The belief that only wealthy people can benefit from whole life insurance is an urban legend that needs to be put to rest.

First off, full disclosure: I’m a financial investigator and an educator, not a licensed financial advisor. I’ve spent the last 25 years investigating more than 450 different financial products and strategies.

Of all of those products, my very favorite is dividend-paying whole life insurance. That’s because it enjoys an unmatched combination of advantages, which include safety, guarantees, liquidity, control and tax advantages.

If you sell dividend-paying whole life, you probably hear many of the same objections to it over and over. But my research has shown these objections are based on myths and misconceptions. So here are the six biggest myths about dividend-paying whole life — and the truth about each of them.

Remember that in financial management, where strategies are pivotal in securing and growing wealth, understanding the nuances of products like dividend-paying whole life insurance becomes imperative. Through Selective Wealth Management, individuals can discern the myths from the realities, leveraging comprehensive financial tools and strategies to optimize their financial well-being. Selective Wealth encompasses a tailored approach that considers individual goals, risk tolerance, and financial aspirations, empowering individuals to make informed decisions and navigate the complex landscape of financial products effectively.

Addressing the misconception surrounding high costs is crucial as it frequently dissuades potential investors. Contrary to this belief, delving into the long-term benefits and the potential for dividends reveals that dividend-paying whole life insurance can be a financially prudent choice over time, particularly when considering Life Insurance rates. By dispelling these myths, investors can gain a more comprehensive understanding of the multifaceted advantages of this type of insurance and its potential impact on life insurance as a whole.

If you don’t sell the product, it may be because you have some of the same objections. Perhaps this will help open your mind…

One of the objections you probably hear about dividend-paying whole life insurance is, “What’s the big deal about dividends? They’re just a return of premium the company overcharged you.”

Recall that dividends are paid when the company’s income less its expenses exceeds its projected worst-case scenario. Technically, the IRS defines dividends as a return of excess premium and therefore not taxable.

However, over time, those dividends can exceed the premium you paid in by a significant amount. If that’s the result of “overcharging,” I say, “Bring it on!”

The financial experts often complain that the insurance company “only pays you the death benefit and keeps your cash value” when the policy owner dies.

Technically that’s true. But how do you explain this: I posted one of my dividend-paying whole life policy statements on our website. It shows how if I’d died on the date the statement was issued, my family would have received a check for $381,776, which is a few thousand dollars more than the original $250,000 death benefit and then-current total cash value ($128,361) combined.

It’s amazing to me that so many people — including many experts — hold whole life insurance to a totally different standard than other financial vehicles. For example, if you have $100,000 of equity in your home and you sell it for $250,000, do you expect to end up receiving both amounts, for a total of $350,000? Of course not.

However, as I just demonstrated, a dividend-paying whole life policy can deliver that advantage.

Financial pundits say that your cash value grows much too slowly in a whole life policy. They claim you might not have any cash value at all in the first couple of years.

True for some whole life policies. However, more and more advisors are incorporating riders that dramatically accelerate the growth of the cash value in the policy, especially in the early years of the policy.

In fact, adding these riders to a policy maximizes both the cash value and the death benefit over time.

In addition, adding these riders allows clients to use their policy as a powerful financial management tool from day one.

Who usually complains the loudest that whole life policies pay too much commission? Often stockbrokers and money managers. They claim that high commissions are the only reason agents sell these policies.

But the reality is that those same money managers are actually making up to ten times as much as an advisor who sells a client a super-charged policy. Let’s compare: Assume you put $10,000 per year for thirty years into a super-charged dividend-paying whole life policy and the very same amount into an investment account.

According to those financial planners and experts, the agent who sold the policy would earn about $10,000 commission in the first year and a small commission each year after that.

That would be true of the policies many advisors design. But because a super-charged whole life policy will direct much of the $10,000 annual premium into the riders that make the cash value grow a lot faster, that advisor will only make between $3,000 and $5,000 in the first year, not $10,000. They’ll receive a small renewal commission during the remaining years, bringing the total commission paid over thirty years to about $8,500.

Meanwhile, the planner or investment advisor who’s complaining that this is way too much commission will earn a management fee every year of at least 1 percent of the account value (and often it’s 1.5 percent or even 2 percent) which, if the market has moderate returns over the same thirty years, means he’ll earn $100,000 – or more!

According to Dr. David Babbel, Professor at The Wharton School of the University of Pennsylvania…

“People don’t buy term and invest the difference. They most likely rent the term, lapse it and spend the difference.”

Professor Babbel is co-author of Buy Term and Invest the Difference Revisited, published in the May 2015 issue of Journal of Financial Services Professionals.

Although much lip has been given to the notion of “buy term and invest the difference,” I’ve never met anyone who actually bought a term policy, priced the cost of a permanent policy with an equivalent death benefit, and then put the difference into an investment account every month. Here are some passive income ideas that can be implemented by everyone that has capacity to generate a steady income all the time.

It just doesn’t happen.

This is an urban legend that desperately needs to be put to rest. Did you know that whole life insurance was part of the financial foundation of half the U.S. population around 1900, and one-third of the population in 1950?

It was common for blue-collar and middle-class families to own these policies. There are folks who have these policies who make $20,000 or $30,000 a year, as well as those who make $300,000 to $3,000,000 per year.

Maybe our grandparents knew something we’ve forgotten?

See also:

9 more things to know about whole life insurance

6 reasons why whole life is causing advisors (and clients) to take notice

Written by Bill Cates | @Bill_Cates

Formal networking groups can be a waste of time or a great opportunity. It all depends on how you “work it.”

I don’t remember who said it, but the saying goes something like “It’s not called net-sit, or net-eat. It’s called net-work.” Here’s a checklist of five habits you want to establish to make the most out of a networking strategy.

This is, by far, the most important item on the list. If your networking colleagues don’t fully understand how you provide value to your prospects and clients, they won’t refer you. And if they don’t like you and trust you, they won’t refer you. You have to have both conditions going for you.

One way to accomplish this is to talk about why you do what you do. Talk about your value in a way that’s personal to you. Tell your story. Provide clear examples. This brings your value to life and fosters a personal connection at the same time.

It’s pretty hard to become referable in short encounters at group meetings. Identify the members who are most likely to know the types of people you want to meet. Then meet with them outside your normal meeting (over a meal is nice).

Make sure you fully understand their value and they fully understand yours. Hint: This often takes more than one meeting.

Just because you give referrals to someone doesn’t necessarily make you referable, but it sure can help. When you do give referrals, practice the Golden Rule of Referrals: give referrals unto others as you would have them be given unto you. In other words, make valuable introductions and strive to create real connections.

Have you noticed how hard it is to reach people these days? Don’t settle for leads or low-level referrals (“Tell him I sent you,” “Here’s the name of a guy who could use your services — give him a call,” etc.) Make sure you arrange an introduction. Then take the next logical step by saying to your referral source, “Let’s talk about how you introduce me to Laura. First, I want you to feel comfortable in doing so. Second, I’d like to pique her interest in hearing from me. Could you say something like … ”

If there’s a “magic bullet” to making networking groups work, this would be it. It’s one thing for you to tout your value. It’s so much more effective for someone else to do so.

The members of your group who have actually experienced your value are the ones mostly like to become your advocates. Once you get one or two, the popcorn starts to pop. More and more members of the group will either want to work with you or feel more confident introducing you.

With this in mind, strive to get at least one new client out of a networking group. Then watch the work roll in.

How do you approach networking? I’d love to hear from you. Send an email directly to me at BillCates@ReferralCoach.com

Click here for the original article.

November 11, 2015 // 8:00 AM

Written by Mike Renahan | @mikerenahan

One of the highlights of working at a close-knit company is getting to spend time with a bunch of professionals in very different functions. I’ve had the chance to learn from marketers, bloggers, developers, public relations experts, people operations managers, sales reps, and many more.

And while it’s been a blast to spend time with everyone, I’ve always enjoyed being near the sales reps. It’s a treat to watch and listen to their interactions with warm prospects, and observe how they spend their time.

Being a sales rep requires you to be a different kind of person. Certain traits make successful salespeople unique in their companies — and sometimes even among their fellow team members. Here are the 11 traits that stood out to me after spending time with some great salespeople.

1) They’re Hustlers

I like to consider myself an early bird, but it looks like I’m late to the office every day when I get here. Each morning, around 7 a.m., our office fills up with salespeople.

The most valuable resource any rep has is time, and this is why they get up early. Several studies have shown the benefits of being an early riser, and great sales reps take advantage of early morning hours to prep for their day and get themselves in the right mindset to sell.

These salespeople also show their hustle by taking failure in stride and trying again. In the world of sales, you’re going to get rejected frequently, and a lot of people can get down on themselves when this happens. Reps that hustle get back on their feet and look forward. They keep moving towards their goals.

Action Steps:

2) They’re Personable

The importance of creating a connection with a prospect and maintaining it once they become a customer has been stressed by countless sales experts. And to build a relationship, you need to be personable. According to Peter Leighton, being personable is universal among people who do well in sales.

When I worked in the same room as sales reps, I was surprised at the number of people that came up and said “hello” to me — even if they didn’t know me. Great sales reps seek out relationships, and want to learn more about their prospects and the people around them. They focus on being approachable, friendly, and open for a conversation.

Action Step:

3) They’re Curious

Curious sales reps are always looking for better ways to be successful, get more done, or solve a problem. They want to learn about the person they are dealing with, their problem, and how they can help. Being curious means you’re hungry for information, which is a critical attribute for sales reps.

Curious people also do something that’s crucial to success in sales today: They ask a ton of questions. Questions not only help sales reps identify the right solution for a prospect’s problem — they also keep buyers engaged.

Action Step:

4) They’re Introspective

One of the things I’ve observed about great sales reps is that they hold weekly meetings to reflect on the previous workweek, and determine what went well, what could have gone better, and where they want to focus going forward. And this self-reflection helps them get ahead. In fact, Allen R McConnell references several studies that cite an introspective attitude’s role in self-improvement.

Great salespeople constantly refine their pitch and their skills. After a successful call, they ask themselves, “What went well, and how do I use that going forward?” After a crappy call, they think, “What didn’t go as planned and how do I adjust to avoid that again?” Remember: You have to reflect on how the process is going in order to improve.

Action Steps:

5) They’re Willing to Experiment

What worked, why did it work, and how do you iterate? Quota-crushing salespeople are constantly asking themselves these questions.

And this means they consistently try new things. They test every little detail in their sales processes: this subject line versus that subject line, this time of day versus that time of day, this question or that question. Great salespeople never settle when they experience a little success. They are always seeking to improve.

Action Steps:

6) They’re Informed

Being informed goes beyond general knowledge of the product. Customers need to trust their sales rep if they’re going to purchase from them. They need to have confidence that you know their industry and what’s best for their business.

This is why great salespeople are always learning, by reading, taking training, participating in events, or participating in some other activity. They make sure they’re always on top of the ins and outs of their prospects’ industry, and have a legitimate answer to every question a buyer might ask.

Action step:

7) They’re Persistent

Rejection sucks, but great salespeople don’t let it get them down. The best reps are persistent about offering their help to prospects to guide them through their purchasing decision.

If salespeople don’t hear back from a prospect, they follow up. If they don’t hear back on the follow up? They follow up again. They don’t give up easily, but they also stay mindful of the razor thin line between being persistent and annoying.

Action Steps:

8) They’re Competitive

The one thing that has stood out to me most since moving to a company with rooms of salespeople is the constant satisfaction they’re after. They’re driving hard to hit their quota faster every single month.

The drive to be the best salesperson in the room is palpable, and the competition is stiff. Ken Sundheim writes in Forbes that in order to be successful in sales, you have to adapt to selling in a highly competitive atmosphere. Great salespeople want to win. They want to close deals, develop relationships, create a strong network of customers, and be successful.

Being competitive is a critical part of sales. It’s often the driving force behind hitting quota month after month.

Action Steps:

9) They’re Patient

Buying decisions take time. Customers now do a ton of independent research before they decide whether or not they’re going to buy. As a sales rep, it’s up to you to work with prospects on their timeframe and help guide them through their decision process.

And this is where patience comes in. In case you doubt the importance of patience in sales, Ayelet Fishbach conducted a study and found that people who are patient, and demonstrate an ability to wait, actually get a larger reward than their less patient counterparts.

Great sales reps don’t pester their prospects every 20 minutes asking if they’re going to buy. Instead, they work on ushering buyers through the funnel on their own time. Patience and sales aren’t normally linked, but in the new playbook, they are. Excellent sales reps focus on delivering a positive experience for the customer above all else.

Action Step:

10) They’re Loyal

Loyalty is the most basic part of the sales relationship. In an article on Psychology Today, Frederick Reichheld argues that the ability to build strong bonds of loyalty — not short-term profits — has become the “acid test” of strong leadership.

Great salespeople stand by their customers. They work with them through the thick and thin and help them achieve their goals — no matter what. In turn, their customers are loyal to them. They’ll continue to purchase their service because they love the loyalty and appreciate the relationship.

Action Step:

11) They’re Independent

Finally, excellent sales reps know how to work on their own. They don’t rely on colleagues to do something for them, or their manager to walk them through a process step-by-step. Great sales reps know that they are their own greatest asset.

John Rampton lists being independent as one of the most important characteristics of people who succeed at sales. A sales rep who can prospect, research, set up meetings, give product demonstrations, maintain relationships, and run experiments all on their own are the ones that are going to be successful.

Action Step:

Being a great salesperson takes time and effort. You have to work at what you want in order to be successful. By doubling down on your strengths and improving your weaknesses, you’ll strengthen your process a little bit each day.

For the original article, click here.

NOV 11, 2015 | BY ROD RISHEL

This is an opportune time to take a fresh look at carriers’ offerings to ensure the most appropriate ones are top of mind.

As we reflect on 2015 and look toward 2016, sea change in America is resulting in a wave of effects on the life insurance industry. From shifts in demographics to Americans’ health status and their sources of retirement income, the new realities are reflected in ways that carriers and their products are transforming to offer solutions.

Let’s explore these new realities and their implications for life insurance product development and distribution.

If you type “millennials” into any search engine, you may get the impression that the millennials are taking over. Article after article explores the many different ways members of today’s most-talked-about generation are leaving their mark on the workforce, the country and the world. While “taking over” might be an exaggeration, it’s not too far from the truth.

The needs and buying habits of millennials differ substantially from prior generations, calling for new approaches in the manner in which life insurance carriers interact with many prospective clients. At the same time, the life insurance business is also evolving to better serve baby boomers, our industry’s traditional primary targets, who are living longer than ever before — although not necessarily more healthfully.

Consider some important truths about millennials — the approximately 83 million Americans born between 1982 and 2000. While not every millennial is the same, the following are three things we know about Generation Y.

First, millennials are a large, and increasingly influential, segment of the population. U.S. Census Bureau estimates for 2015 indicate that millennials now represent 25 percent of the U.S. populace, making them our nation’s single largest demographic group.

Pew Research Center analysis of this data indicates that millennials surpassed Gen Xers in the first quarter of 2015 to take over the largest share of the American workforce. Look around you: More than 1 in 3 U.S. workers today is a millennial.

Second, many millennials have already fallen behind in planning for their financial futures. According to a 2015 LIMRA Secure Retirement Institute study, 70 percent don’t know how much they ought to be saving for retirement, and only four in 10 are putting aside at least 10 percent of their incomes. Websites like myprivatehealthinsurance.com provide great health insurance coverage, but more than half of the millennials are not even aware of that.

Given the fact that this generation grew up in an era of great financial flux — coupled with the reality that they’re currently paying down burdensome student loans, getting married, starting families, taking on mortgages and more – it’s no surprise that long-term financial planning isn’t necessarily a top priority for millennials as they head into 2016.

It is surprising, however, that 15 percent of millennials think winning the lottery is a “viable retirement strategy” and 11 percent are hoping for monetary gifts to see them through their later years.

That’s according to a 2015 study by the Insured Retirement Institute and the Center for Generational Kinetics. The report also finds that 70 percent of millennials underestimate — by about $10,000 per year — how much money they’ll need to spend in retirement.

Third, when it comes to life insurance specifically, millennials are woefully underserved and, perhaps, undereducated. Recent LIMRA research indicates that while a majority believe they need to have more coverage, fewer than one in five are “very likely” to buy it.

In fact, in a 2015 study from Life Happens and LIMRA, 60 percent of millennials prioritize paying for mobile phones, Internet and cable over life insurance. Saving for vacations is more important to 29 percent.

In the year ahead, what will be the best way to get millennials to rethink these priorities and begin to understand the role life insurance serves in protecting their financial futures? Ideally, millennials will be met in the marketplace on their own time and terms, as they will likely help steer their own buying experiences.

Part of the key to meeting millennials on their own time and terms lies in understanding how their lives and spending habits have been shaped by technology. Millennials can search for and buy something on their smartphones or laptops in less than a minute, and believe everything should be that quick and easy.

They are exposed, primarily on the Internet, to abundant information about whatever they are buying. They expect to be able to “visit” their financial professionals and their accounts anytime they want, virtually or electronically, 24/7.

To connect with this demographic group in 2016, insurance carriers and financial professionals should focus on natural, straightforward communications. It will be crucial to be able to relay the value proposition of the solutions being offered, and to be able to provide more information, in an easily palatable format.

When it comes to specific products, what is most appropriate for some millennials (as determined after a comprehensive financial assessment that should be conducted for each client or prospect) may be a universal life insurance policy offering not only needed guarantees, but also the potential to access cash value in the contract to cope with costly contingencies while still alive.

Just because millennials have risen to the top of the demographic charts this year doesn’t mean it’s time to push the needs of baby boomers to the back burner. Far from it.

Baby boomers are the wealthiest generation in American history. Older boomers are nearing retirement and younger boomers are beginning to confront the challenges of aging. As they evolve, boomers will continue to reshape every aspect of life they touch.

Their own lives have been shaped in part by their journey through economic recession. Having seen the impact that hard times can have on personal and family finances, many boomers are still working. In fact, according to the Pew Research Center Fact Tank, of the 75 million Americans born between 1946 and 1964, about 45 million are still in the labor force as 2016 approaches. Furthermore, boomers are known for their work ethic. If you’re going to be doing business with them in the coming year, they’re likely going to want to see that same quality in you. You can also read more to know the complete details that they have planned to make the changes.

Many of these Americans are living longer than ever and facing new challenges, such as supporting aging parents and adult children who may have moved back home. These situations tend to put significant pressure on boomers’ finances and retirement savings.

Furthermore, today’s pre-retirees anticipate shifting income sources in retirement, as LIMRA shared in an October 2015 report. The report noted that, “While 5 percent of retirees consider income from defined contribution (DC) plans to be the primary source of income for their households, 21 percent of pre-retirees expect DC plans to be their primary source of retirement income.

This shift toward greater distributions from DC plans and IRAs presents a challenge for future retirees, as securing a sustainable income has become an individual responsibility.”

Given the retirement income challenge, it’s not surprising that, as relayed in an August 2015 news release from the Insured Retirement Institute, only 27 percent of recently surveyed baby boomers express confidence in their retirement savings, a 5-year low. Forty percent say they have no retirement savings at all. There seems to be no reason to expect drastic improvement in those figures in the coming year.

While concerns persist about insufficient retirement income, Americans are also grappling with chronic illnesses that may contribute to their need for costly long-term care. According to a May 2015 report from the U.S. Centers for Disease Control and Prevention, baby boomers are dealing with more stress and more health issues compared to the same age group 10 years ago. And they face a growing risk of developing chronic health problems.

It seems clear that, as financial and insurance planning continues with clients in 2016, product development initiatives in our industry will need to acknowledge that baby boomers need flexibility, too. These clients need life insurance solutions that answer the traditional need to protect family finances and leave a legacy, but also provide a means of addressing policyholder needs during — or even before — retirement.

How are carriers transforming life insurance products to address the needs of both demographic groups: baby boomers as well as millennials? Two examples of innovation in action include:

Some carriers are also leveraging what they’ve learned in the development of global life insurance and non-life products to create unique product offerings. And they’re listening closely to what clients and financial professionals alike are saying about what constitutes a truly great buying experience.

Due in part to initiatives such as these, the market now features a number of recently introduced or retooled living benefit riders on life insurance, with the goal of providing multipurpose solutions for clients whether they consider themselves in the “social media generation” or closer to the “Social Security generation.” (Not that Grandma and Grandpa aren’t on Facebook, too.)

Consider accelerated benefit riders for chronic illness. When educating clients about them in 2016, be cognizant that their payout structure may be newly updated. Riders such as these, when purchased with some index universal life and guaranteed universal life products, allow access to cash value in the policies (in qualifying circumstances under the terms of the riders) to help clients pay for assisted living, nursing home care, adult daycare and more.

This type of solution aims to help clients protect themselves and their families as they age and increasingly bear the costs of health care. Likewise, longevity riders with some universal life insurance products can provide a guaranteed stream of income in retirement, enabling clients to overcome the real possibility that they may outlive their savings.

Essentially, longevity riders transform life insurance into a solution that’s intended to both meet a family’s financial needs if the worst should happen (by providing a death benefit) and offer a source of retirement income if the best should happen (the client lives to age 85 or beyond, with as few as 15 years having passed since the purchase of the policy).

Some recent, well-structured universal life products have featured dual living benefit riders — one for chronic illness and one for longevity — with a goal of meeting clients’ needs whether they die too soon, live too long, or become seriously ill along the way.

As solutions evolve along with client needs, however, financial professionals may want to consider whether, depending on each client’s individual circumstances, having just one or the other of these powerful types of riders on the policy may be sufficient to meet the identified needs.

By taking into account not only the importance of a death benefit — but also offering the potential to access an accelerated portion of that death benefit to help cover the cost of life’s contingencies — living benefit riders serve a pivotal role in a modern, overall balanced approach to financial and retirement planning. They leverage a permanent life insurance product for protection, flexibility and control while living, helping to protect against life’s most formidable risks and offering a meaningful value proposition for Americans of any generation.

As our industry prepares for 2016, there’s every reason to believe ongoing change in America will continue to result in product development that’s more attuned to the needs of clients across the age spectrum. This is an opportune time to take a fresh, in-depth look at carriers and their offerings to ensure the most meaningful and appropriate solutions are top of mind, whether the prospective policyholders are millennials, baby boomers or “in betweens.”

See also:

Off the beaten path tips about saving money (from a millennial)

Financial picture brightens for millennials (but not boomers)

Millennials highly optimistic about insurance industry, plan to stay as long as possible

November 11, 2015 // 8:30 AM

Written by Dan Tyre | @dantyre

Top salespeople are successful because they sweat the details. They probe for pain, help their prospects, and run effective sales calls. They listen closely to what their prospects say, effectively determine the right solution, and ask for help when they need it.

Top reps are articulate, forceful, and direct. And most importantly, they don’t use weasel words.

“Weasel words” are words or phrases that subliminally undermine your credibility. Salespeople sometimes use weasel words to try and appear important, but prospects can see right through them, which undermines your trust and impacts your ability to close a deal.

Word choice on a sales call? Isn’t that a little control freak-ish?

No way. Think about it — every word you say to a prospect is an opportunity to bolster or weaken your credibility, so top salespeople choose their words carefully. Below are the top five phrases that undermine your credibility.

You might as well put a sign on your forehead that says, “I’m a bonehead.”

This phrase is a colloquialism that calls to mind the old-time salespeople you see in infomercials selling you detergent at 3:00 a.m. on cable. You come off as disingenuous (or even slimy) because you have to ask for trust in a passive-aggressive way. If you’ve already established trust with your prospect, you never need to say this — they will implicitly put stock in your words.

It also comes across as a condescending brush-off. Saying “Trust me” gives the impression that you’re glossing over something, don’t really want to explain the answer to your prospect’s question, or think they won’t understand it. It’s a deflection tactic that will arouse suspicion in your prospects, who will think, “What’s he hiding from me?”

Everything that’s wrong with the phrase “Trust me” applies here as well. But saying “To be honest … ” has additional problems.

Your prospects will think, “Wait, what? So she wasn’t being honest in the first 25 minutes of the call?”

Like trust, honesty shouldn’t be something that needs to be explicitly addressed. It should be there from the beginning, and specifically calling attention to the fact that you’re being honest now throws all your other conversations into a suspicious light.

Well, can you or can’t you?

It’s okay to be uncertain, but it’s not okay to glide over a question and leave it unanswered. Instead, acknowledge that your prospect has asked you a interesting question (yes, literally say the words, “That’s a great question!”), and let them know that you’ll find the answer and send them follow-up resources.

Don’t undermine yourself by making up a quick answer that might be wrong. An incorrect answer that you give now will be far more damaging to your authority than having your prospect wait a few hours for the right one.

This is just flat out offensive! Anyone who asks this question should be dragged out of the sales profession immediately. If your prospect isn’t the sole decision maker, you’re going to make them uncomfortable — not to mention you’re suggesting they’re not worth talking to unless they are a decision maker, which is both shortsighted and rude. This question is a great way to condescend to somebody. Stay away!

As a salesperson, you’re immersed in your own industry. You’re familiar with all the lingo and inside language. But remember that the acronyms and phrases you take for granted are probably foreign to your prospects.

Don’t get myopically focused on what you know and assume that your prospect is on the same page. You should be able to explain these concepts in a simple way, so do it! Using jargon might make you feel smart, but it’s just going to confuse your prospect.

There’s too much chance in sales to risk screwing up a deal because you chose your words sloppily. Always aim to be open, honest, and forthright, and avoid words and phrases that will endanger your prospect relationships and your reputation.

For the original article, click here.

NOV 12, 2015 | BY SHEP HYKEN

Take care of your clients and the money will follow.

I recently had the chance to interview Tariq Farid, the founder and CEO of Edible Arrangements. If you aren’t familiar with Edible Arrangements, it is like a flower shop, but instead of flowers, they sell and deliver bouquets of fresh fruit.

The company originally began as a flower shop when a neighbor loaned Tariq the money to open the business while he was still a teenager in high school. He quickly repaid that loan and started to expand into what is now a 1,200 unit international franchise organization. Ivy Kids is also providing franchise opportunities at affordable deal.Hence you can also make use of it.

Tariq shared stories about how he “wowed” his customers with a level of service that allowed him to compete and win in a very competitive business. He walks the talk, having created a simplistic three word mission statement, which is “To Wow You!”

In addition to using customer service as his competitive weapon of choice, he grew his business by listening to his mother’s sage advice: Don’t chase money!

What that means is that if you care more about the money than the customer, you won’t always make the sale. And if you do make the sale, you might not keep the customer long term.

So what does it really mean to put the customer before the sale? I think it is best summed up with a personal story about a shopping experience I had several years back.

I went to the mall to buy a shirt that was advertised to be on sale. Unfortunately, the store was sold out of the shirt in my size. The salesperson picked up the phone and called the other stores in the area, but to no avail.

None of their stores had the shirt. That’s when the salesperson called a competitor in the mall. She found the shirt, in my size, and had the store hold it for me. Pretty impressive! Her effort earned her my loyalty.

I once heard a similar story. Everything was exactly the same except for the ending. Rather than send the customer to the competitor’s store to pick up the item, the salesperson asked the customer to come back in about fifteen minutes. The salesperson went to the other end of the mall, bought the shirt from a different store, and brought it back to sell to the customer. It didn’t matter that the store didn’t make any money on that sale. What mattered is that the salesperson took care of her customer. In addition, effective fintech digital marketing strategies can help fintech firms reach their target audience and achieve business growth.

I’ve been a believer of this concept since the beginning of my career. The late Dr. Theodore Levitt, professor at Harvard Business School, used to say, “The function of a business is to get and keep your customers.”

If you ask people, “What is the function of a business?” most will say, “To make money.” Unfortunately they are wrong. Making money is the goal, and if you confuse the function with the goal, you may not hit your goal.

If you’re looking to expand your business internationally and reach clients abroad, Acclime Singapore offers valuable assistance and support every step of the way. And if you’re in the legal industry, partnering with a specialized Lawyer Marketing Agency at https://fwd-lawyermarketing.com/ can ensure that your marketing efforts are just as effective on a global scale. So, don’t chase the money—chase the customer!

Sign up for The Lead and get a new tip in your inbox every day! More tips:

The evolution of customer service

The formula for building relationships that last

Local: (937) 890-4991 Toll Free: (800) 762-7500 Fax: (937) 890-1909